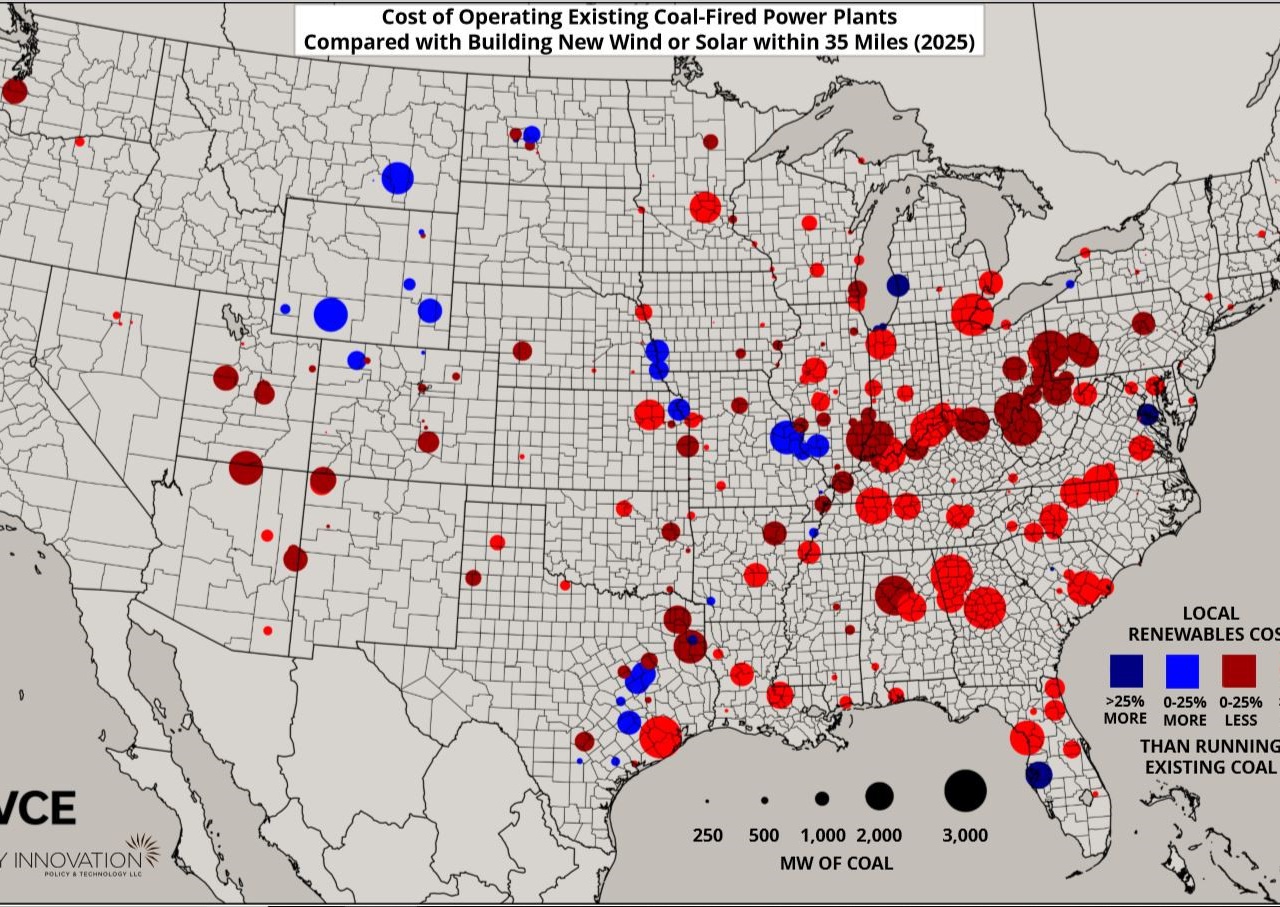

Research shows the United States hit a “coal cost crossover” point in 2018 where simply operating two-thirds of existing coal-fired generation costs more than replacement with new wind or solar within 35 miles of those plants. By 2025, that number rises to three-quarters of existing coal-fired generation, rendering uneconomic tens of billions in coal assets.

These assets are roughly analogous to corporate loans gone bad, but with risks passed onto consumers. Though utilities may have bet wrong on lifespan estimates for coal investments, most plants are monopoly-owned, enabling cost-recovery from captive customers absent regulatory intervention.

But how fast utilities can refinance or securitize these toxic assets (already underway in multiple states), and how much customers pay, depends heavily on depreciation — a process to restructure and pay off these assets using arcane accounting rules.

Maximizing the public interest through depreciation requires understanding these rules, choices available and tradeoffs of differing approaches. Ultimately, how depreciation is decided helps to determine the economics of a coal-to-clean transition.

Refinancing early-retired coal plants to save money

The electric utility sector is divided between competitive electricity markets where generation owners assume risks that power plants will become uneconomic, and markets where monopolies own generation and receive regulatory assurances of cost recovery for investments.

Coal generation in competitive markets has taken a hit as ever-cheaper renewable energy gains market share at coal’s expense. But in monopoly markets, where coal receives regulatory protection, the coal-to-clean transition has been confronted by regulatory barriers.

Rather than responding to competition, regulated coal retirements are “scheduled” for the end of each plant’s projected useful life, based on engineering estimates. Each subsequent capital investment (such as air pollution scrubber retrofits to comply with Clean Air Act regulations) then gets its own useful life estimate and related depreciation schedule, extending the plant’s useful life through new investments and increasing amounts of utility capital subjected to a new schedule.

Monopoly utilities and state legislatures are setting aggressive decarbonization goals, exacerbating coal plant risks in these markets and forcing early retirement considerations.

When plants retire before the end of their useful lives, regulators must account for remaining book values on utility “plant in service” accounts, many of which still hold significant dollar amounts. Remaining book values of retired plants will stay in consumers’ rates until regulators consider changing them by re-examining depreciation and finding ways to refinance unpaid balances to reduce consumer costs.

Adjusting depreciation schedules can have outsized utility rate impacts depending on balances that remain to be paid. So, depreciation schedules determine the starting point for regulatory discussions about refinancing the remaining balances outstanding for early-retired coal plants.

Revised depreciation then determines how much and when consumers will pay for remaining investments after the retirement of uneconomic coal plants.

Understanding depreciation cost accounting

Depreciation accounts for tangible asset costs over useful lives, and recognizes reduced asset value over time.

For example, a power plant in operation for ten years has less value than a new one. However, depreciation is an abstraction with real dollar implications, not an asset valuation method. It allocates costs to relevant accounting categories and determines how assets’ balance sheet values change over time.

Depreciation cost accounting, measuring declining asset value over time, allocates original cost over service life under federal or state regulatory agency discretion.

For monopoly utilities, it also includes already-recovered cumulative depreciation costs in a “depreciation reserve” account combining investment return and “rate base” valuation deductions. The market value of tangible assets determines the rate base value on which a utility is entitled to earn a fair and reasonable shareholder return — critical for determining that utility’s revenue requirement, investor rates of return, and ultimate price for power charged to customers.

If the depreciation rate increases to accommodate an earlier retirement time schedule, annual depreciation costs will increase as demonstrated in the utility revenue requirement equation above.

Accelerating depreciation has a similar impact to reducing mortgage payback time — higher monthly payments expedite amortization and decrease total interest earned by the bank (or rate of return for the utility), while reducing total consumer cost of paying off the asset.

Using depreciation to determine remaining value of early-retiring coal plants

Depreciation schedules define how much investment must be addressed when plants retire early, impacting how much (and over what time period) customers pay for these assets. Instead of presenting fixed amounts with little opportunity for adjustment, depreciation can be changed in three ways:

- Once determined, depreciation value can be adjusted.

- Depreciation schedules can be lengthened or shortened.

- Amounts included or excluded in depreciation can accommodate a variety of plant and plant-related investments and expenses.

Adjusting depreciation is important because end-of-life dates are based on engineering estimates of equipment lifespan under normal circumstances. Plants will likely carry remaining undepreciated balances because utilities are provided incentives by regulation to invest more in plants to earn equity returns whenever they can justify such investments.

An illustrative timeline of the impacts of accelerated depreciation on the value remaining in utility rates

Accurately determining values at stake in early plant retirements requires a recent regulatory determination of remaining plant depreciation — similar to requiring a recent home valuation to refinance a mortgage.

If depreciation has not been recently reviewed for a plant under consideration for early retirement, utilities and stakeholders can question remaining investment amounts at stake — particularly if they have subsequently invested additional capital in a plant.

Depreciation is typically reviewed every five years, and both amounts subject to depreciation and length of time an asset’s costs are depreciated can change. Resolving differences among depreciation approaches, particularly in the context of looming coal plant retirements and refinancing, through securitization or otherwise, requires balancing contrary interests.

From depreciation to regulatory asset

After depreciation reviews are completed for early retiring plants, public utility commission orders define amounts remaining in new “regulatory asset” accounts, providing the starting point for refinancing and securitization discussions.

Regulators must choose between allowing plants to become regulatory assets or disallowing recovery in rates in whole or in part. Since early retired plants are no longer “used and useful” for customers, remaining unpaid plant balances can be removed from a utility’s rate base.

If the decision is to allow recovery, remaining unpaid plant balances can be placed in “regulatory asset” accounts. Disallowance is usually unpalatable for utilities, their investors and regulators, depending on plant investment circumstances, and is more typically considered when utilities have shown clear planning, investment or operational malfeasance.

Comparing the relative costs of capital for securitized debt, corporate debt, equity, and regulator-authorized returns on equity.

Regulatory asset accounts track total remaining asset values included in rates to pay off remaining utility investments after plants retire, and are subject to depreciation. Equity portions of these accounts usually receive the same regulated rate of return as plant-in-service asset equity.

In other words, utility shareholders may make money off unpaid investment in a retired plant, though this rate of return is also adjustable.

Depreciation adjustments also reopen debate over real-world market values and costs of uneconomic coal plants.

Negotiations for early plant retirements and asset valuation must also consider demolition costs, plant salvage value and plant site remediation. These can be difficult to predict since they depend on construction costs which vary over time along with interest rates, material costs and cyclical factors that increase or decrease costs depending on when estimates are made.

Balancing differing interests in depreciation

Regulators confronting competing claims and equities have many opportunities to balance and compromise among disputes in depreciation — and options for reasonable compromises abound for asset valuation and depreciation timelines to satisfy utilities, consumers and clean energy advocates.

- Utilities: Accelerating depreciation to match early retirement dates appeals to utilities because it improves cash flow by charging depreciation expense to consumers at higher rates, reducing non-performing or uneconomic asset perceptions among investors, and limiting risks of holding regulatory assets to shorter periods of time. However, accelerating depreciation also reduces future utility returns. Utilities with negligible uneconomic asset risks may seek to maintain their regulated asset account value on the original depreciation schedule. Given the certainty that accelerating depreciation allows utilities, depreciation schedule compromise is often possible to accommodate utility expectations.

- Consumers: Accelerating depreciation to match early retirement dates confronts consumers with short-term rate increases, which they generally oppose. Any rate change must be tempered with concerns over rate certainty, rate change moderation, and potential for consumer backlash. The relative cost responsibility between current and future consumers also causes tension. Future consumers should not bear the brunt of paying off assets current customers use or from which they will not benefit. Other lower-cost financing options become even more important for balancing consumer interests — using low-cost debt to pay off undepreciated assets provides additional savings to ameliorate consumer equity and cost concerns.

- Environment: Clean energy advocates may argue that regulators should consider whether depreciation changes expedite or stall early fossil plant retirements. Accelerated depreciation matching cost recovery with cost responsibility makes the coal-to-clean transition more expensive in the near term. Advocates may argue transition benefits like front-end fuel savings justify spreading depreciation costs across more time so future ratepayers share cost responsibility, since they will pay lower fuel costs through their use of more clean energy.

Depreciation’s role in the coal-to-clean transition

There is no magic formula to balance all competing equities through depreciation. Because of the expertise and information needed for effective depreciation accounting, these discussions are often dominated by utilities and regulatory staff.

As more stakeholders get involved in the coal-to-clean transition, understanding these impacts and potential options for balancing interests in depreciation accounting, as well as related tradeoffs and opportunities inherent in refinancing, will be essential for maximizing public interest outcomes through these proceedings.